In a poignant and gripping presentation at St. Joseph’s University, New York’s Long Island Campus, Carlos Sanchez shared his harrowing journey of what he maintains was a wrongful murder conviction,…

“Speed doesn’t matter. Forward is Forward.” That’s what SJNY Online‘s Tracie Esposito’s graduation cap is going to say on it this May as she crosses the stage at commencement —…

Faculty NewsLong Island

Faculty NewsLong IslandFederal Court Pretrial Officer Shares Expertise with Criminal Justice Students

A U.S. Pretrial Services Agency officer spoke with dozens of criminal justice majors this semester during a presentation in the Long Island Campus’ Shea Conference Center. Mallori Brady, who works…

Alumni NewsBrooklynFeaturedLong IslandOnline

Alumni NewsBrooklynFeaturedLong IslandOnlineStephen Somers ’82 Honors Legacy with $1M Scholarship Gift

Driven by his passion to make a positive impact in the lives of others and to give back to an institution that he credits with transforming his life, alumnus Stephen…

Eunah Lee, Ph.D., first became interested in philosophy during high school. She found herself mesmerized while reading Korean-translated excerpts from German-American philosopher Herbert Marcuse in her literature class. Now, Dr.…

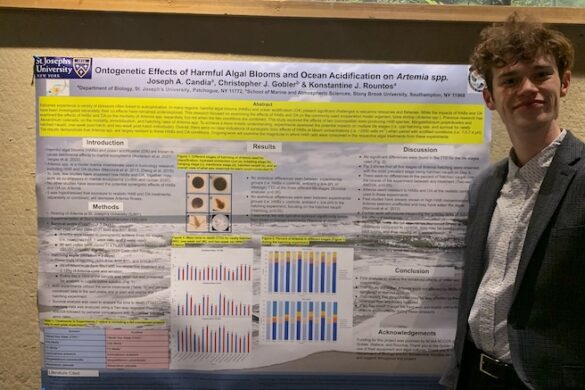

SJNY senior Joe Candia ’24 has taken advantage of the many opportunities provided to St. Joseph’s students for hands-on learning. After spending last summer as a research student with Konstantine…

Corned beef and cabbage, bagpipes, and lots and lots of green. St. Joseph’s University, New York alumni gathered Sunday, March 3, at the Dyker Beach Golf Course in Brooklyn for…

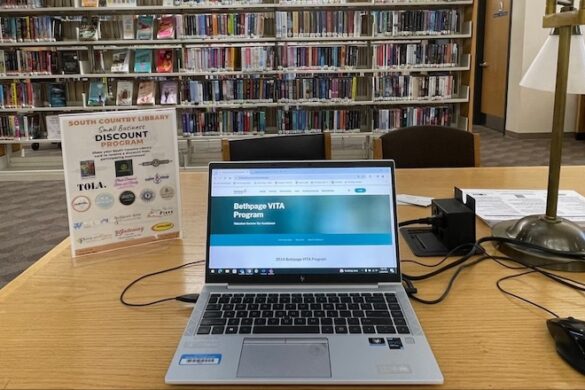

Student volunteers from St. Joseph’s University, New York are participating in a community outreach effort that is providing free income tax preparation services for low and moderately income residents of…

Alumni NewsBrooklynI Heart SJC Week

Alumni NewsBrooklynI Heart SJC WeekBuilding a Bond Beyond the Court: Billy ’06 and Kristin Haufmann ’06

From their high school days at Christ the King in Queens to their college years at St. Joseph’s University, New York’s Brooklyn Campus, William “Billy” Haufmann and his wife Kristin…

Home SJNY Magazine

Newer Posts